![]()

|

|

|

Amortized Loan - How to Calculate Loan Amortization using Present Value Interest Factor An amortized loan is one that is paid off in equal periodic instalments or payments and includes varying portions of principal & interest during its term. Examples of amortizable loans include auto loans, mortgages, business loans & others. How do you compute the periodic payments on an amortized loan? The formula is:

Where:

How to calculate the amount of loan: 1) Divide the principal loan amount (A) b PVIFA, which is a factor shown in the Present Value Interest Factor of Annuity of $1 table, and use this formula

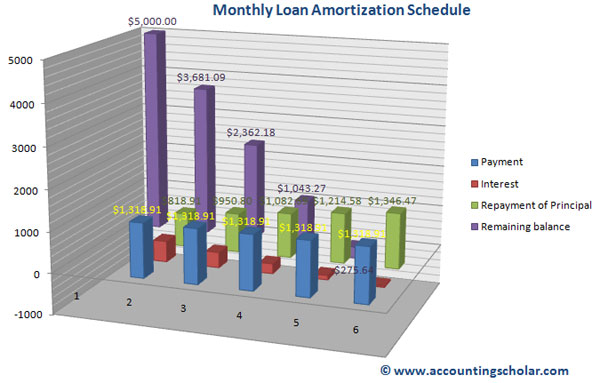

Example Consider a firm borrows $5,000 to be repaid in five equal instalments at the end of each of the next five years. The discount rate on this loan payable is 10%. What is the amount of each instalment payment?

Once the monthly loan instalment is computed, a loan amortization schedule can be created and each loan payment consists partly of interest & principal. The interest portion of the payment is usually the largest during the first few periods because the loan amount is highest at that point in time. However, as instalments are made and the loan balance decreases, the interest payments become lower as the interest rate is updated with the ending balance of the loan amount. Confused? We derive an example below:

* Note the interest in Year 1 is calculated by multiplying the ending balance, $5000 by 10% which totals $500. In year 2, interest is calculated by multiplying the ending balance $3,681.09 by 10% which is $368.11. ** Repayment of Principal (D) = (B) – (C) ----We know that the total monthly payment will be $1,318.91, thus the repayment of principal amount is Payment – Interest.

Mortgage lenders who work for banks & financing companies

use this amortization formulas and methods to determine the periodic mortgage

payments & break them down in to principal & interest reductions.

This information is also used by consumers who need a breakdown of their

monthly payments, and how much of that goes in to interest & how much

balance goes towards their principal.

|

© Accounting Scholar | Privacy Policy & Disclaimer | Contact Us |