![]()

|

|

|

Dividend Growth Model - How to Value Common Stock with a Constant Dividend and "No Growth"

This implies that the dividend payout in Year 2 will be the same as the dividend payout in Year 1, and likewise the dividend payout in Year 3 will be the same as in Year 4, thus D remains constant. Therefore, we can tweak this formula to come up with a new common stock valuation formula:

Since the dividend is always the same, the stock can be viewed as an ordinary perpetuity with a cash flow equal to D every period, thus the per-share valuation of the common stock is given by this formula:

Where:

As an example, consider Cofta Corp. has a policy of paying $20 per share dividend every year, and the company expects to continue paying out this dividend indefinitely. What will be the value of a common share of stock if the required rate of return is 15%?

What if we knew the dividend for this company always grows at a steady rate every year. We will call this growth rate g. If we let D0 be the dividend just paid, then the next dividend D1 will be:

Where:

Having said this, what is the formula for dividend payout in 2 periods?

We can repeat this process to come up with the dividend at any point in the future. Thus, the dividend Dt in t periods in the future is given by:

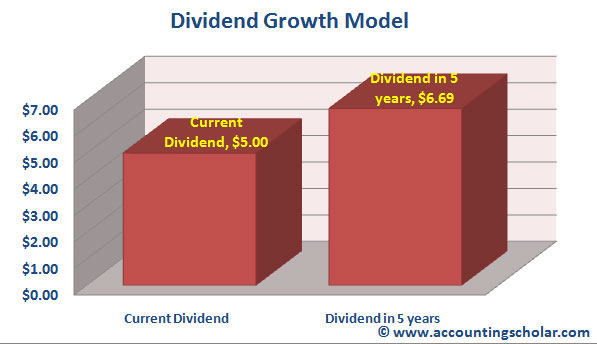

Example of Dividend Growth TD Dominion bank has just paid a dividend of $5 per share and the dividend grows at a steady rate of 6% per year. Based on this information, what will the dividend be in 5 years?

Thus in 5 years, the dividend will grow from $5 per share to $6.691 thus growing a total of ($6.691 - $5) = $1.691

|

© Accounting Scholar | Privacy Policy & Disclaimer | Contact Us |

How

do we value common stocks for which we know the future prices 2 to more

years or periods down the line? For instance, we may be able to estimate

what a stock will be worth 2 years from now, and this does not fit our

current formula where P1 equals the price of the stock in one year or

period. Here’s how to solve this problem. A common stock in a company

with a constant dividend is much like a share of preferred stock because

the dividend payout does not change. Financial managers also know that

the rate of growth on a fixed-rate preferred stock is zero, and thus is

constant through time. For a zero growth rate on common stock, thus D1

will be:

How

do we value common stocks for which we know the future prices 2 to more

years or periods down the line? For instance, we may be able to estimate

what a stock will be worth 2 years from now, and this does not fit our

current formula where P1 equals the price of the stock in one year or

period. Here’s how to solve this problem. A common stock in a company

with a constant dividend is much like a share of preferred stock because

the dividend payout does not change. Financial managers also know that

the rate of growth on a fixed-rate preferred stock is zero, and thus is

constant through time. For a zero growth rate on common stock, thus D1

will be: