![]()

|

|

|

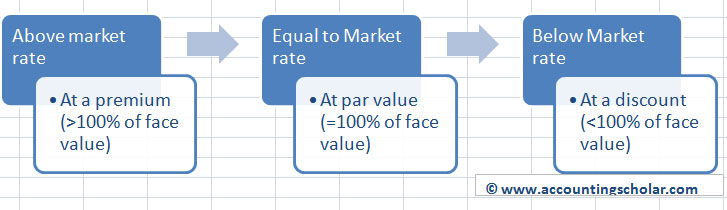

Premium on Bonds PayableDifference between par value of a bond and its higher issuing price is known as a premium on bond payable and arises when the contract (coupon) rate is higher than the bond’s market rate. The market rate of interest (effective interest rate) is the % of interest borrowers are willing to pay and lenders are willing to earn for a certain bond taking in to account its risk level. When the bond contract rate equals the market effective interest rate, the bond trades at par value or 100%. When the contract rate does not equal effective interest rate, the bond trades above or below par value; the summary is shown in the table below. Bond Premiums & Discounts - Contract Rate versus Market Rates

|

© Accounting Scholar | Privacy Policy & Disclaimer | Contact Us |