![]()

|

|

|

Chapter 3.2® - Example of Net Realizable Value less a Normal Profit Margin, Market equals = Net Realizable value or Market equals net realizable value minus a normal Profit Margin

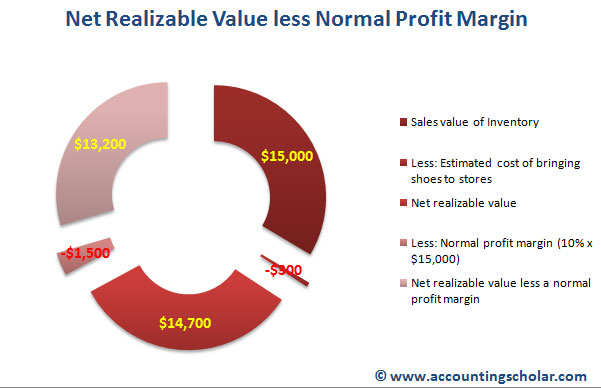

Let’s consider an example where we lower the carrying value of inventory using the net realizable value less a normal profit margin method. Consider a sporting goods company owns shoes worth $13,500 at December 31st, 2009; these shoes have a selling value of $15,000. The estimated cost of bringing these shoes to its stores for resale is $300 and a normal profit margin is 20%. How do we determine “market” in such a case?

This pie graph shows a break down of the sales value of inventory less estimated costs of bringing the shoe inventory to stores & the net realizable value. A normal profit margin is deducted of the net realizable value to arrive at 'net realizable value less a normal profit margin.' Let's consider 2 scenarios where in i) Market equals Net Realizable value and ii) Market equals net realizable value minus a normal profit margin. i) Market equals = Net Realizable value If market equals the net realizable value alone, then we see that with an original purchasing cost of $13,500, there will be a $1,200 gain reported on the income statement, in the form of reduced cost of goods sold ($13,500 - $14,700) because instead of reporting Cost of Goods Sold of $14,700 which is the market, we will recognize the original purchasing cost of $13,500 as COGS and deduct this from Net Sales. In 2011, when we record $13,500 as the cost of inventory (due to lower of cost or market with cost being lower at $13,500), we will realize a gain of $1,200 on the shoes inventory after deducting the cost of resale of $300.

ii) Market equals = Net Realizable Value minus a Normal Profit Margin In the second example where market equals the net realizable value minus a profit margin, there will be a $300 loss reported on the income statement in 2010 because we are using the lower of cost ($13,500) or market ($13,200), thus we are using the market. Notice however that we benefit in 2011 because when subtracting this $13,200 market from revenue, we derive a profit of $1,500. If we had used the higher cost of $13,500, we would be short $300 profit because the calculations would look like:

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

© Accounting Scholar | Privacy Policy & Disclaimer | Contact Us |