![]()

|

|

|

Chapter 2.2® - Example of Return on Equity & Raising Capital through Bonds & Shares and its Effects on Return on Equity - Issuance of Common Shares versus Bonds Payable

Let’s consider Shab Networks Corp has income before tax of $200,000 and has no interest expense. The company has $1 million in equity and is planning a $500,000 expansion to meet increasing demand for its products/services. Shab Networks predicts this $500,000 investment will result in additional net income of $135,000 per year before paying interest or taxes. Shab Networks sat down with its board of directors and Controllers group to discuss this issue and considered 3 options:

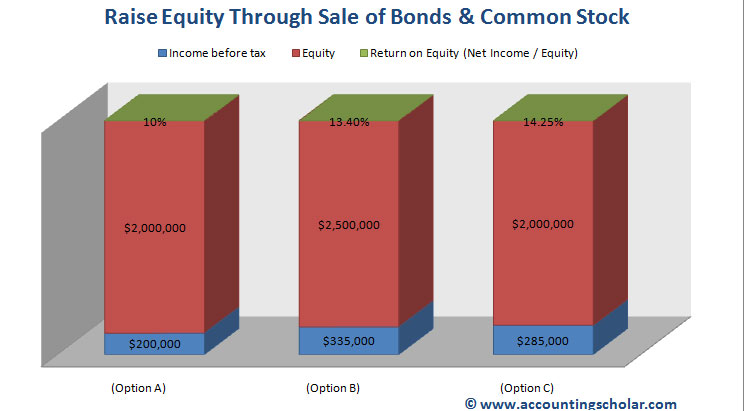

Tabular Analysis of Income before Taxes & Interest Expense

The tabular analysis above shows the corporation will earn a higher return on equity (14.25%) if it expands by issuing $500,000 worth of bonds, even though its net income is lower than Option B, totalling $285,000 while Option B has net income of $335,000. Thus, the best option for this organization is option C which is to sell $500,000 worth of bonds and paying a 10% annual coupon rate with an interest payable of $50,000 per year.

This above graph shows the raise of $500,000 via common class stock (Option B) & its associated rate of return of 13.40%. It also shows raise of capital via bond issuance and its return of 14.25%. Note that the income is higher under Option B of common stock issuance ($335,000) while the issuance of bonds yields a net income of $285,000 however the return on equity calculation (net income / equity) is higher for Option C due to the $500,000 bond payable allocated to the liabilities section of the balance sheet, as opposed to it being put under shareholder's equity under Option B; you can verify this by checking the equity is $2,500,000 under Option B while it is $2,000,000 under Option C. |

© Accounting Scholar | Privacy Policy & Disclaimer | Contact Us |