Financial

forecasting is an essential part of all financial planning of a

corporation as it is the basis for budgeting activities and estimating

future financing needs of the company. Financial forecasting typically

involves forecasting sales and expenses incurred to generate those

sales. When making a financial forecast, directors typically use

an estimate of various expenses, sales & liabilities and the

most widely used method for making such projections is the percent-of-sales

method. In the percent of sales method, assets, liabilities &

total expenses are estimated as a percentage of sales that are then

compared with projected sales. These numbers are then used to design

a pro forma (panned or projected) balance sheet.

The steps necessary to compute a pro forma balance

sheet is as follows:

1. Express balance sheet items that vary directly

with sales as a percentage of sales. Any items that do not vary

directly with sales e.g. long term debt, retaining earnings, common

stock & property/plant/equipment are designated as not applicable

(n/a).

2. Multiply the percentages from step 1 by the sales

projected to obtain the amounts for future periods.

3. Where no percentage applies (e.g. for long term

debt, common stock or retained earnings numbers), take the figures

from the present balance sheet in the column for the future period.

4. Calculate the projected retained earnings using

the below formula:

Projected Retained Earnings = Present

retained earnings + Projected Net Income – Cash Dividends

Paid

5. Total up the assets account to obtain a total projected

assets number, then add projected liabilities & equity accounts

to determine the total shortfall. This shortfall indicates the total

external financing that is required to keep the company running

at present operational levels.

Example of Financial Forecasting Using Percent

of Sales Method

Let’s do a financial forecast for Bongo Corp.

for the year 2009 assuming net income is to be 10% of sales and

the dividend payout ratio is 5%. Also, projected sales are estimated

to be at $60 million (using an estimate of 2 x current assets).

The

forward market allows investors to trade forward contracts on currencies

on the global currencies markets. A forward contract is an agreement

between an organization and a commercial bank to exchange a specified

amount of one currency at a specified exchange rate (also known

as the forward rate) on a specified date in the future. Why would

a corporation ever need a forward contract? Consider a multinational

corporation operating in Finland anticipates a future receipt of

foreign currency such as the Chinese Yuan from a customer in China.

When such a need arises, the multinational corporation can lock

in the rate at which they purchase or sell a particular foreign

currency.

This is known as hedging a currency. Usually forward

contracts involve very large corporations expecting merchandise

from a foreign currency and expecting to pay the supplier in their

local currency. Therefore, a typical forward contract is valued

at a minimum of $1 million US. Thus, forward contracts are normally

not used by small corporations or individual investors. When a large

corporation goes to obtain a forward contract, and if the bank has

a doubt in its ability to make future payments, the bank could ask

for a small upfront deposit to ensure the corporation will be able

to repay. This type of a deposit is known as a compensating balance

and no interest is received on any sums deposited. Most common forward

contracts are for 30, 60, 90, 180 or 360 days.

How International Companies Use Forward Contracts

Multinational corporations use forward contracts to

hedge their expected imports. They can lock in the rate at which

they will be able to obtain a currency needed to purchase imports

from a foreign country. As an example, consider Mike Tee Corp. operating

out of Orlando, Florida will need $1,000,000 Australian dollars

to purchase their imports of raw materials. It can purchase Australian

dollars, at say $0.60 per Australian dollar. At this spot rate,

the firm would need:

Australian Dollars = $1,000,000

Spot rate = $0.60 per Aussie dollar

American funds needed = $1,000,000 Australian

x $0.60

American funds needed = $600,000 US

However, let’s assume the company does not have

$600,000 US to buy their imports now. The company can wait for 90

days and raise the cash needed, and exchange it to Australian dollars

at the spot rate available during that time. But we do not know

what the spot rate will be during that time. Say in 90 days, the

Australian dollar rises to $0.65 for every $1 US as a result of

the Aussie government increasing interest rates. When this happens,

Mike Tee Corp. will need additional funds to purchase the same $1miillion

Aussie dollars. Here are the calculations:

Australian Dollars = $1,000,000

Spot rate = $0.65 per Aussie dollar

American funds needed = $1,000,000 Australian

x $0.65

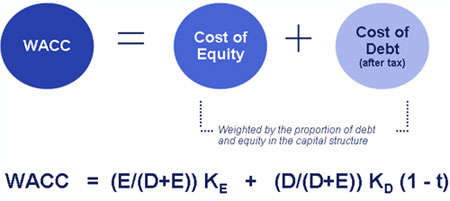

Weighted

Average Cost of Capital is a calculation of the overall cost of

capital used by a corporation and is an average representing the

total return (in percent) that is expected of an organization on

all its assets, debts and owner’s equity to maintain its current

stock price & valuations. Weighted Average Cost of Capital weighs

in all items that play a role in the corporation’s capital

structure including common and preferred shares, bonds, and other

long term debts.

In order to calculate the weighted average cost of

capital, we must first examine the capital structure of the company

we are analyzing. In terms of corporate finance, capital structure

refers to how a corporation finances it assets and its business

operations; either through the use of long term debt, common shares

or preferred stock (also known as shareholder’s equity) or

other hybrid securities. Weighted Average Cost of Capital becomes

especially important when the capital structure of a firm involves

both debt and equity financing. In this example, we will look at

the three most common types of financing included in capital structure:

i) Common shares equity

ii) Preferred shares equity

iii) Long term debt

Steps for Calculating Weighted Average Cost

of Capital

There are three steps for calculating the WACC of

an organization.

1) Determine the proportionate weighting

of each source of capital financing based on their market

value.

2) Calculate the after-tax rate of return

or cost of each source.

3) Calculate the weighted average cost

of all sources

The formula for WACC is:

WACC = (Ke x We) + (Kp x Wp) + Kd/pt

[1 – t] x Wd)

Ke =Cost of capital -common

equity

We =Percent of common equity

in the capital structure, at market value

Kp = Cost of preferred equity

(shares)

Wp =Percentage of preferred

equity in the capital structure (at market value)

Kd/pt =Cost of debt (pre-tax)

T = Tax rate

Wd=Percentage of debt in the

capital structure (at market value)

Sales to Accounts Payable = Sales / Accounts Payable

ii) Days’ Purchases in Accounts Payable

Days’ purchases in accounts payable = Accounts

Payable / (Purchases / 360 days)

Assume the following data derived from the Income statements &

Balance sheets of Juakali Corp. for its 2009 year.

2009 (Year 1)

2010 (Year 2)

Accounts Payable

$76,500

$71,300

Purchases

$900,000

$845,000

Sales

$2,100,000

$1,800,000

The relevant ratio calculations for each of the years

are:

2009 (Year 1)

2010 (Year 2)

Sales to Accounts

Payable

$2,100,000 / $76,500 = 27.45

$1,800,000 / $71,300 = 25.25

Days’ Purchases

in Accounts Payable

$76,500 / ($900,000 / 360)

= 30.60 days

$71,300 / ($845,000 / 360)

= 30.38 days

Notice that the sales to accounts payable ratio went

down from 27.45 in Year 1 (2009) to 25.25 in Year 2 (2010); an improvement

of 8%. This indicates the company’s improved ability in year

2 (2010) to obtain short term credit & financing in cost-free

funds. This ratio simply means the company is making more sales

and is lowering its accounts payable by a certain percentage, which

is good for investors & the outlook for the balance sheet. Below

we present the data in graphical format. (View

Full)

Dollar

Cost averaging is an investment mechanism in which stocks are purchased

at constant dollar amounts at regularly spaced intervals, with the

most amount of stocks bought at the lowest stock prices possible.

By investing a fixed amount of money each time, more shares are

bought at lower prices and fewer shares are bought at higher prices.

This approach results in a lower average cost per share because

the investors buy more shares of the same stock at the lower prices.

The formula for dollar cost averaging is: (View

Full)

Dollar Cost Averaging (Average Price)

= Total market price per share / Total number of Investments

Example

An investor invests $200,000 per month in IBM shares

and performs the following transactions:

Most

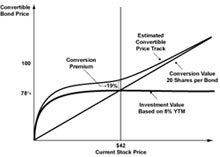

newbie investors are confused as to what convertible bonds are;

they wonder are they really bonds or convertible bonds that are

stocks, or both? Basically, convertible bonds are corporate bonds

(bonds issue by large organizations) that are convertible in to

the common stock of that issuing corporation. Convertible bonds

are when bondholders can exchange their bonds for a fixed number

of the issuing company’s common shares. Convertible bonds

allow bondholders the potential to increase their net worth by future

increases in the market value of the common shares of the issuing

company. If the share prices of the company do not increase and

the bonds are not converted, bondholders will continue to receive

periodic interest payments and their principal amounts upon maturity.

Bond Conversion Ratio

The bond conversion ratio is also known as the conversion

premium and ultimately determines how many shares can be converted

from each bond outstanding. This conversion can be expressed as

a ratio or as the conversion price. Usually the details regarding

this are stated in the bond’s agreement or indenture.

As an example, consider Jahmani Corp. offers bonds

with a conversion ratio of 32:1 for their bonds with a $1000 par

value. This means each bond outstanding (with a par value of $1,000)

can be exchanged for 32 shares of the issuing company’s common

shares.

Let’s consider a hypothetical bond conversion

example to clarify the conversion process & accounting rules.

Assume that Jahmani Corp. is issuing a new bond to the market with

a 6% coupon rate and 10 years to maturity. The company has other

10 year term debt that carries an 8% yield and the company’s

stock price is currently trading at $41. Here is a summary of this

data in tabular format

Annual

percentage rate (APR) is a true measure of the interest fees charged

by credit card companies & banks. Annual percentage rate (APR)

is the effective cost of credit which is the ratio of finance charges

to the average amount of credit used in the life of the loan; this

is expressed as a percentage per year. In this tutorial, we look

at the calculation of APR for single payment loans & multiple

instalment loans.

Single Payment Loans

A single payment loan is repaid in full on the maturity

date and there are two ways of calculating APR on single loan payments:

I) simple interest method and ii) the discount method. The difference

between the simple interest method & the discount method is

what the borrower actually receives in the form of a loan.

i) Simple Interest Method

Under the simple interest method, interest is calculated

on the full original amount borrowed. The formula for simple interest

is:

Simple interest = Principal x Rate x

Time = p x r x t

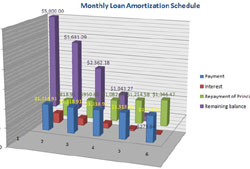

An

amortized loan is one that is paid off in equal periodic instalments

or payments and includes varying portions of principal & interest

during its term. Examples of amortizable loans include auto loans,

mortgages, business loans & others. How do you compute the periodic

payments on an amortized loan?

The formula is:

Amount

of loan = A = (P / PVIFA)

How to calculate the amount of loan:

1) Divide the principal loan amount (A) b PVIFA, which

is a factor shown in the Present Value Interest

Factor of Annuity of $1 table, and use this formula

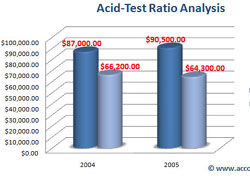

The

acid-test or quick ratio is a variation of the current ratio that

divides current assets by current liabilities to arrive at an answer.

However, it is a stricter test of a company’s liquidity because

it factors in to account only the most liquid assets that a company

has including Cash, short term investments & accounts receivable.

Inventory is not included in the acid-test ratio calculation because

of the length of time needed to convert inventory to cash by making

sales. However, there may be some types of inventories such as groceries,

milk, eggs & meat that are more liquid than accounts receivable,

however according to accounting standards; they may not be included

in the acid-test ratio. Also, prepaid expenses are not included

in the acid-test ratio because they cannot be converted in to cash

and are not capable of covering current liabilities...

Weighted

Average Cost of Capital is a calculation of the overall cost of

capital used by a corporation and is an average representing the

total return (in percent) that is expected of an organization on

all its assets, debts and owner’s equity to maintain its current

stock price & valuations. Weighted Average Cost of Capital weighs

in all items that play a role in the corporation’s capital

structure including common and preferred shares, bonds, and other

long term debts.

Weighted

Average Cost of Capital is a calculation of the overall cost of

capital used by a corporation and is an average representing the

total return (in percent) that is expected of an organization on

all its assets, debts and owner’s equity to maintain its current

stock price & valuations. Weighted Average Cost of Capital weighs

in all items that play a role in the corporation’s capital

structure including common and preferred shares, bonds, and other

long term debts.  Most

newbie investors are confused as to what convertible bonds are;

they wonder are they really bonds or convertible bonds that are

stocks, or both? Basically, convertible bonds are corporate bonds

(bonds issue by large organizations) that are convertible in to

the common stock of that issuing corporation. Convertible bonds

are when bondholders can exchange their bonds for a fixed number

of the issuing company’s common shares. Convertible bonds

allow bondholders the potential to increase their net worth by future

increases in the market value of the common shares of the issuing

company. If the share prices of the company do not increase and

the bonds are not converted, bondholders will continue to receive

periodic interest payments and their principal amounts upon maturity.

Most

newbie investors are confused as to what convertible bonds are;

they wonder are they really bonds or convertible bonds that are

stocks, or both? Basically, convertible bonds are corporate bonds

(bonds issue by large organizations) that are convertible in to

the common stock of that issuing corporation. Convertible bonds

are when bondholders can exchange their bonds for a fixed number

of the issuing company’s common shares. Convertible bonds

allow bondholders the potential to increase their net worth by future

increases in the market value of the common shares of the issuing

company. If the share prices of the company do not increase and

the bonds are not converted, bondholders will continue to receive

periodic interest payments and their principal amounts upon maturity. Annual

percentage rate (APR) is a true measure of the interest fees charged

by credit card companies & banks. Annual percentage rate (APR)

is the effective cost of credit which is the ratio of finance charges

to the average amount of credit used in the life of the loan; this

is expressed as a percentage per year. In this tutorial, we look

at the calculation of APR for single payment loans & multiple

instalment loans.

Annual

percentage rate (APR) is a true measure of the interest fees charged

by credit card companies & banks. Annual percentage rate (APR)

is the effective cost of credit which is the ratio of finance charges

to the average amount of credit used in the life of the loan; this

is expressed as a percentage per year. In this tutorial, we look

at the calculation of APR for single payment loans & multiple

instalment loans. An

amortized loan is one that is paid off in equal periodic instalments

or payments and includes varying portions of principal & interest

during its term. Examples of amortizable loans include auto loans,

mortgages, business loans & others. How do you compute the periodic

payments on an amortized loan?

An

amortized loan is one that is paid off in equal periodic instalments

or payments and includes varying portions of principal & interest

during its term. Examples of amortizable loans include auto loans,

mortgages, business loans & others. How do you compute the periodic

payments on an amortized loan? The

acid-test or quick ratio is a variation of the current ratio that

divides current assets by current liabilities to arrive at an answer.

However, it is a stricter test of a company’s liquidity because

it factors in to account only the most liquid assets that a company

has including Cash, short term investments & accounts receivable.

Inventory is not included in the acid-test ratio calculation because

of the length of time needed to convert inventory to cash by making

sales. However, there may be some types of inventories such as groceries,

milk, eggs & meat that are more liquid than accounts receivable,

however according to accounting standards; they may not be included

in the acid-test ratio. Also, prepaid expenses are not included

in the acid-test ratio because they cannot be converted in to cash

and are not capable of covering current liabilities...

The

acid-test or quick ratio is a variation of the current ratio that

divides current assets by current liabilities to arrive at an answer.

However, it is a stricter test of a company’s liquidity because

it factors in to account only the most liquid assets that a company

has including Cash, short term investments & accounts receivable.

Inventory is not included in the acid-test ratio calculation because

of the length of time needed to convert inventory to cash by making

sales. However, there may be some types of inventories such as groceries,

milk, eggs & meat that are more liquid than accounts receivable,

however according to accounting standards; they may not be included

in the acid-test ratio. Also, prepaid expenses are not included

in the acid-test ratio because they cannot be converted in to cash

and are not capable of covering current liabilities...