![]()

|

|

|

Chapter 1.4® - Methods of Amortizing Capital Assets - Straight Line Amortization, Units of Production & Double-Declining balance (Accelerated Amortization method)

Methods of Amortization There are 3 ways of amortizing Capital assets over their useful lives. We shall describe each one in depth below.

i) Straight Line Amortization Straight-line amortization expenses the same amount to expense each period over the useful life of the capital asset. There is a 2 step process used to calculate the amortization expense:

The simple formula is summarized as:

Consider BB Company purchased a high-end computer on January 1st, 2004 for $15,000 and used it throughout its predicted useful life of 5 years, through to December 31st, 2008. The salvage value is expected to be $3,000.

Here is the accounting entry to be made at the end of December 31st, 2004, after using the computer for 1 year.

The debit to Amortization expense appears on the Income Statement in the Operating expenses section. The Credit to Accumulated Amortization appears below the Computer Equipment Asset account as a Contra-asset account. Remember through Accumulated Amortization, we are keeping track of the reduction in value of the Computer Asset control account. This is why accumulated amortization is a contra-asset account. Here’s how these entries are reflected on the Balance sheet.

In order to save space on the balance sheet, many organizations list the Computer Equipment asset net of accumulated amortization. This means the accumulated amortization has already been subtracted from the asset account, here’s how it looks.

From the schedule, we note that:

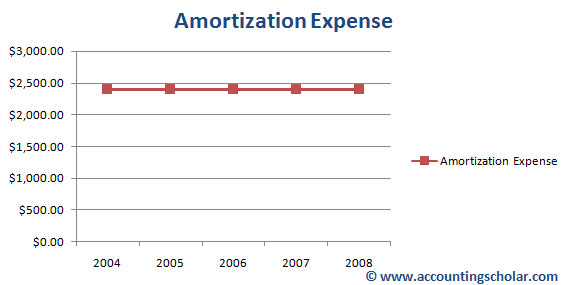

This chart shows the linear amortization

expense of $2,400 per year that the company incurs; this amortization

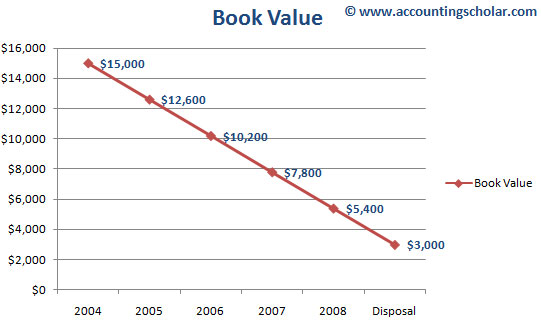

expense is recorded on the Income statement as a non-cash expense. This chart shows the decline in book value (recorded value) of the capital asset declining at a pace of $2,400 per year on a linear basis. Note the graph shows that the ending book value of the asset will be $3,000 in 2008 and beyond upon which it is disposed.

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

© Accounting Scholar | Privacy Policy & Disclaimer | Contact Us |