![]()

|

|

|

Chapter 2.8® - Straight Line Amortization Method of Bonds Payable & Bond Amortization Schedule versus Effective Interest Method of Bonds Amortization

The straight line method of amortization allocates interest expense equally over the life of the bonds (over the 6 interest payment periods). To calculate this number, we divide $232,740 by 6 giving us a total bond interest expense of $38,790 per period. Alternatively, we can derive this number by adding the $30,000 semi-annual interest payments + ($52,740 / 6 periods) = $8790 totalling $38,790 per period. The accounting journal entry to record this is:

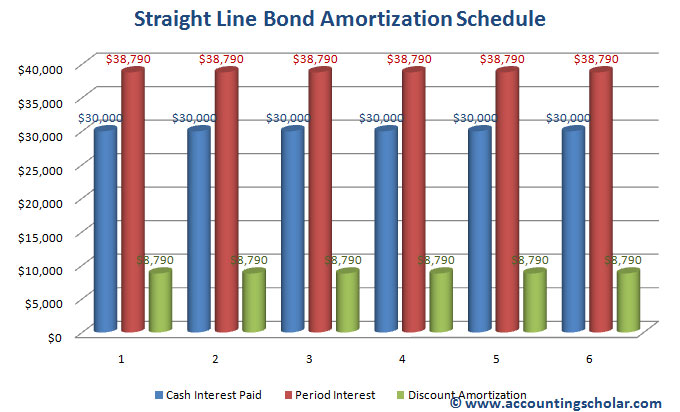

The company incurs a $38,790 bond interest expense each period but only pays out $30,000 in cash because the remaining $8,790 will be repaid when the bond becomes due. This $8,790 credit to Discount on Bonds Payable account increases the bonds’ carrying value because it is a contra-asset account, which is subtracted from the Bond Payable account. The below table shows the decreases in the Discount on Bond Payable along with increase in bond’s carrying value each period. Straight Line Bond Amortization Schedule

*Note that upon the end of the life of the bond payable (December 31st, 2011), the unamortized discount equals $0. **Note that the carrying value of the bond upon the end of its life (December 31st, 2011) becomes equal to par value of $1,000,000.

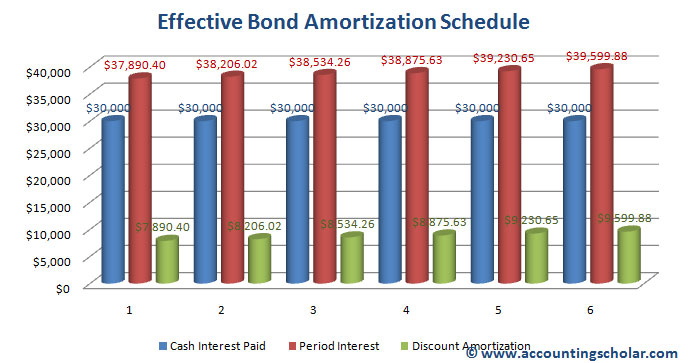

This graph shows the monthly cash interest payments allocated in to the total interest payment (the static $30,000) and $8,790 that is amortized from bond discount. As you can see, the figures remain the same throughout the 6 payment periods due to the straight-line amortization method. Below, you will see the numbers will change for the effective interest method because we will be amortizing the discount on bonds payable at effective market interest rate, instead of a constant rate. Effective Interest Method for Amortization of Bonds Payable In the straight line amortization method, the bond’s carrying value changes each period while the bond interest expense each period remains the same. This displays a changing interest rate when the carrying value fluctuates each period while interest remains the same. Thus, the accounting handbooks advise to only use this rule when the results do not differ significantly from the effective interest method. The effective interest method allocates bond interest expense over the life of the bonds in such a way that it yields a constant rate of interest, which in turn is the market rate of interest at the date of issue of bonds. With effective interest method, the bond payable and discount/premium is calculated using the effective market interest rate versus the coupon rate used in straight-line method. Below is the amortization schedule for this bond issue using effective interest.

Note: We have a $403.16 unamortized discount because of rounding issues, but normally most companies would use automated amortization schedules that will take care of rounding issues leaving no variance. Also note that the interest expense charged each period (Column C) changes from period to period and is not static as in the straight line method. The accounting journal entry made to record bond interest expense on June 30th, 2009 is:

This graph (above) shows the bond amortization schedule calculated using the effective market interest rate as opposed to the Straight-line amortization method (above) that uses the static bond coupon rate to calculate the monthly interest payments. The effective interest method allocates bond interest expense over the life of the bonds in such a way that it yields a constant rate of interest, which in turn is the market rate of interest at the date of issue of bonds. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

© Accounting Scholar | Privacy Policy & Disclaimer | Contact Us |