Just like how we calculated the present value of future

annuity payments now, we can calculate the vice versa meaning we can calculate

the future value of cash flow payments (PMT) given a present value today.

Remember in these calculations, we do not need the Future value (FV) information.

Let’s take an example; suppose you want to start up a new business

and need $100,000 to start up, market and run your business. Because you

feel the business will be short lived for some reason, you would like

to pay off this $100,000 balance in a set of five equal payments. Given

the interest rate is 14%, what will your monthly annuity payments (five

of them) be?

Notice in this example we know the present value is $100,000

and the interest rate on the loan is 14%. Since these payments are spread

over 5 periods and the payments will be equal, what will the payments

be? We will use the present value of an annuity formula to derive our

answer:

Annuity Present Value = C x [(1

– Present Value Factor) / r]

$100,000 = C x [(1 – $1/

(1 + r)t) / r]

$100,000 = C x [(1 – $1/

(1 + 0.14)5) / 0.14]

$100,000 = C x [(1 – $1/

(1.93) / 0.14]

$100,000 = C x [(1 – 0.518)

/ 0.14]

$100,000 = C x [(0.482) / 0.14]

$100,000 = C x 3.443

C = $100,000 / 3.443

C = $29,044.44

This therefore means you will have to make annuity payments

of $29,044.44 every year for the next 5 years to pay off the $100,000

loan at 14% interest rate.

Here’s how to do this exact calculation using our

BAII plus financial calculator:

Find annuity PMTs of $100,000 PV at Year 5, 14% borrowing

rate using our Financial Calculator

N

=

5

I/Y =

14%

PV =

$-100,000

PMT =

?

FV =

$0

2ND

I/Y

P/Y =

1

C/Y =

1

CPT & PV =

$29,128.35

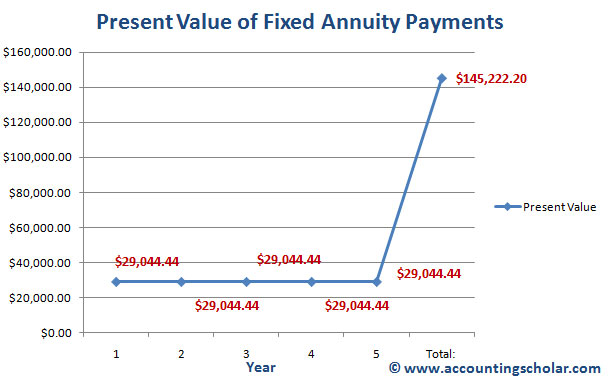

Below is a graphical representation of this data.

This graph above shows the equal annual payments

of $29,044.44 that will pay off the entire loan in 5 years at 14% interest

rate. The graph also indicates to us that the total cost of the loan would

be $145,222.20 which indicates total interest will be $145,222.20 - $100,000

= $45,222.20